As insurers shift to digital platforms, they gain access to more business opportunities and customers touchpoints than ever before. In underwriting, technology has allowed underwriters to reduce their administrative workload and manual efforts. However, this shift to digital has also led to an increase in issues such as:

- Complex risk profiles,

- High transaction volumes,

- Indigestible data,

- And a rise in potential fraudulent online claims.

To remain competitive in this digital market, insurers need to focus not only on delivering the best possible quotes for their customers, but also keeping their overall risk exposure at the ideal level. Fortunately, there are many data tools available in the market to help with both goals. By learning how to identify useful data and leverage business insights tools, insurance underwriters can better monitor their risk portfolio and guarantee the accuracy of their quotes.

This blog addresses the challenges in underwriting processing and shows how Power BI and data analytics tools can be used for underwriter business insights.

Major Challenges With Underwriting Processing

Underwriters today deal with the pressure to make underwriting decisions as quickly as possible, while still improving the consistency and quality of their results. When it comes to underwriting, insurers face three major challenges: complicated risk profiles, upfront quoting, and insurance fraud activities.

Understanding Complicated Risk Profiles

Today, underwriters find themselves dealing with a higher volume of complicated risk profiles, wherein they must consider a large amount of data for each case, often in complex and unstructured forms. Third party and social media data are available, but underwriters haven’t figured out how to maximize benefits from it. This increase in data volume makes it difficult to identify the relevant information for evaluating the amount of risk the company is taking on overall, and as a result underwriters lose their understanding of the company’s risk exposure.

Upfront Quoting Accuracy

Customers nowadays are able to shop around for quotes online, which has increased competition and demand for quick and easy quoting. They want reasonable quotes with minimal back-and-forth, while insurers want to make sure they fully cover their risk. This can be challenging when case situations are more complex and underwriters are overwhelmed with the number of cases.

Increase in Fraudulent Information

The anonymity of the internet and diversity in insurance input systems has led to an increase in fraud, misrepresentation of information, hiding of priors and legal offenses, and fake identities. With more and more automation and no-touch processes, underwriters have to oversee more channels of information and more fraud slip by. Underwriters have to keep up to date on growing trends in fraudulent behavior without affecting their relationships with legitimate customers.

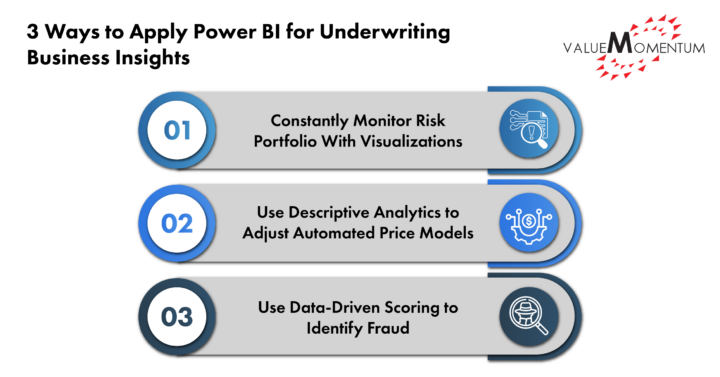

3 Ways to Apply Power BI for Underwriting Business Insights

By using analytics on underwriting data, insurers can gain insight into their risk portfolio, improve the accuracy of their quotes, and detect instances of fraud. Here are three ways underwriters can find solutions using business insights:

1. Constantly Monitor Risk Portfolio With Visualizations

Underwriters need to gain a high-level view of their risk portfolio, and ensure it is within the risk appetite of the insurance company.

Business insights tools like Power BI have dashboard and data summary tools designed for to give underwriters an overarching view of their risk profile, including different risk types and ratings.

The software can provide charts, maps and tables to help underwriters identify patterns in their data, while providing access to data sources for requirements and performance dashboards presented in-line during the process. For example, underwriters can use Power BI to leverage geospatial data and analyze if they are too heavily concentrated in one area or region before any calamities occur.

By viewing the condition of the broader risk portfolio, underwriters can decide if aggregate exposure of the portfolio is in need of recalibration, or if their insurance company needs to take on reinsurance as well.

2. Use Descriptive Analytics to Adjust Automated Price Models

Underwriters need to provide their customers with accurate quotes based on their specific situations and improve the speed of delivery.

Automating more typical or straightforward underwriting cases using straight-through-processing has been helpful for many insurers looking to improve the speed of delivery. In order to stay up-to-date, insurers can leverage descriptive analytics to understand patterns and design algorithms that make decisions based on the insurer’s criteria. By automating the underwriting for some cases, underwriters then have more time to grapple with complex cases and focus on building relationships with customers and distributors instead.

3. Use Data-Driven Scoring to Identify Fraud

Underwriters need to be able to score each transaction for fraudulent activity such as rate evasion. Intelligent business software like Power BI leverages pre-built AI and ML models for effective fraud management that use predictive analytics to detect patterns by examining historical trends. This allows underwriters to generate scores that indicate and predict the likelihood of fraud as online quotations, applications, and policy transactions increase.

Streamlining Insurance Underwriting With Business-First Analytics

Underwriters are under enormous pressure to understand the likeliness of the event they are insuring against, the external threats that may change or increase the risk, and what any serious negative impacts could be. The most forward-thinking underwriters will use data sources and advanced technologies to dynamically calculate their risk profiles and constantly improve and streamline their underwriting processes, so they are ready to tackle any future complications.

Value Momentum’s DataLeverage team have the expertise and experience to facilitate legacy transformation and modernization, while taking a comprehensive approach to data-driven strategies. Using our strong understanding of insurance data models, we can help you leverage technology to better serve your customers and stay competitive in the market.

Ready to improve business insights for business functions at your company? Check out our Data & Analytics services to learn how we can help you leverage modern data tools to upgrade your business strategies.